Weekly Crypto Card Intel

Fee changes, new cards, cashback drops — delivered weekly. Plus a free PDF: Top 10 Crypto Cards Ranked by Real Fees.

No spam, ever. Unsubscribe anytime.

Why your foreign transactions cost more than you think, and which cards actually have no hidden markup.

I run a database of every crypto debit and credit card I can find. 170 of them so far, from Coinbase down to obscure neobank wrappers nobody has heard of. It lives in the Sweepbase catalog if you want to poke around.

One thing kept bothering me. Nearly every card on a landing page says “0% FX fees.” The actual cost of a foreign purchase is all over the place. I went through the fee schedules of all 170 cards and tried to pull out the real total cost of a single transaction abroad. Here is what I found.

| Card | Value |

|---|---|

| 0% FX | 49 cards |

| 0.01–1% | 37 cards |

| 1.01–2% | 36 cards |

| 2.01–3% | 12 cards |

| 3%+ | 6 cards |

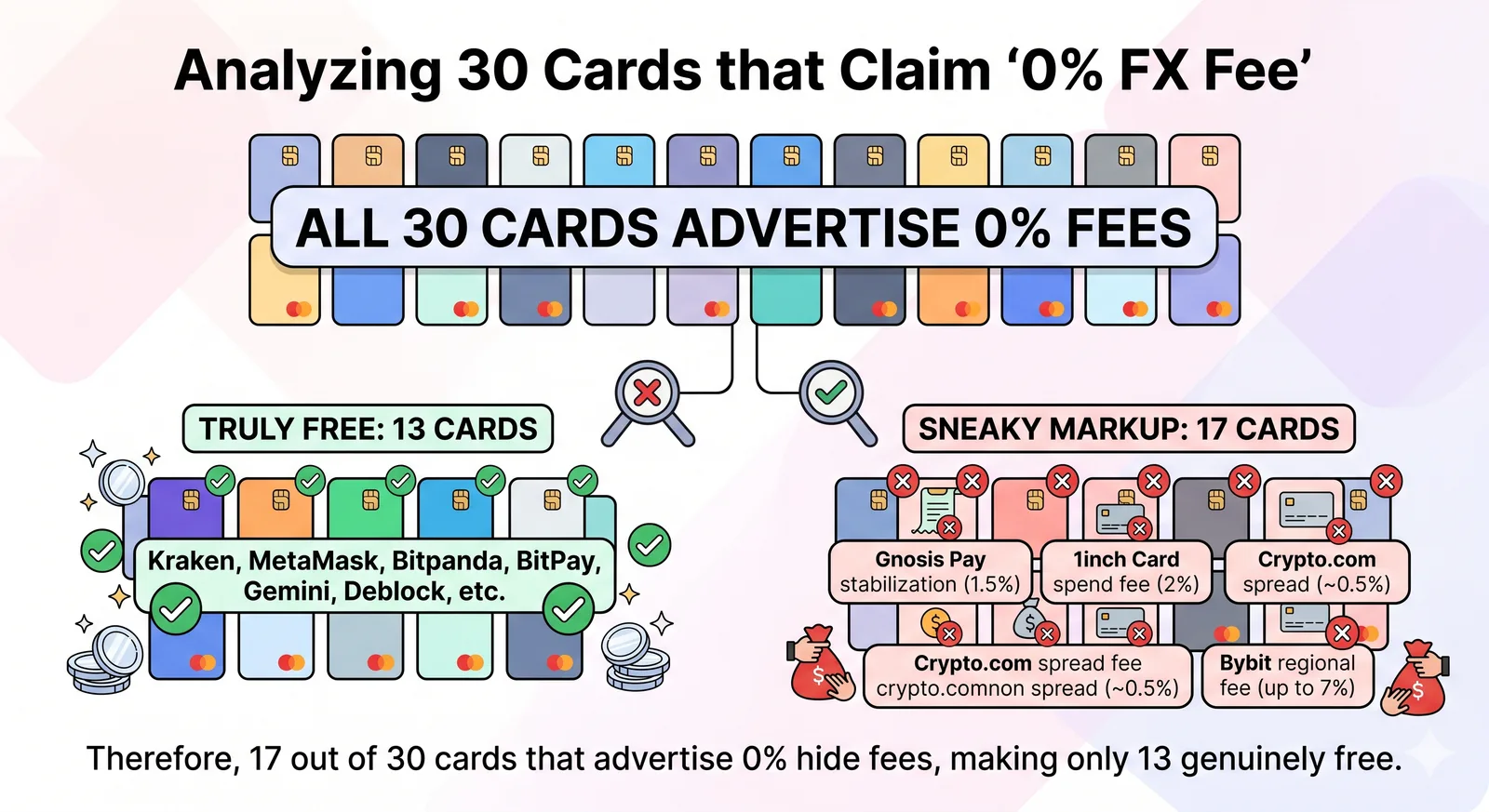

The 0% bucket looks comfortable until you remember 15 of those cards have a hidden markup. We hand-audited the fee schedules and judged 7 to be genuinely clean; the rest sit in a "have not yet read line-by-line" middle.

The first version of this analysis was supposed to be a simple count: how many of the 169 cards I could read a fee schedule for advertise a 0% FX fee. The answer is 49. The follow-up question is the one that took me a month to answer: do those 49 cards actually charge 0%. 15 of them, on a careful read, do not. They charge something on FX, but the something is rebranded. The most common rename is "network fee", which is true in that Visa and Mastercard charge a network markup on cross-currency settlement, but it is also misleading because most other cards quote that network markup inside the FX-fee number. Two issuers split the markup into a "FX adjustment" and a "settlement spread" line on the statement, which together run higher than a clean 1% FX on competitor cards.

I am not suggesting any of this is illegal. Every issuer in the table discloses the rename inside a help-center article, usually two clicks deep from the marketing page. The point of the analysis is to show how much variance there is once you take the "0% FX" claim at face value and read the fee schedule against an actual cross-currency transaction.

“FX fee” is one line item on a long fee schedule. When issuers take it off that line, they usually re-bill the same cost under a different name. Here is the gap between what is on the landing page and what you actually pay once you read the full terms:

| Card | Advertised | Actual cost per foreign transaction |

|---|---|---|

| 1inch Debit Card | “0% FX” | 1.75% crypto-to-fiat conversion fee per transaction |

| Crypto.com Visa | “0% FX markup” | ~0.5% conversion spread on crypto-to-fiat |

| Wayex | “0% FX” | 1% crypto-to-AUD on every purchase and ATM |

| Bitrefill | “0% on EUR” | 1.99% conversion if you fund with crypto |

| Avici | “0% Avici fee” | Visa’s ~1% International Service Assessment still applies |

| Wirex | “0% FX all tiers” | Spread on crypto-to-fiat conversion |

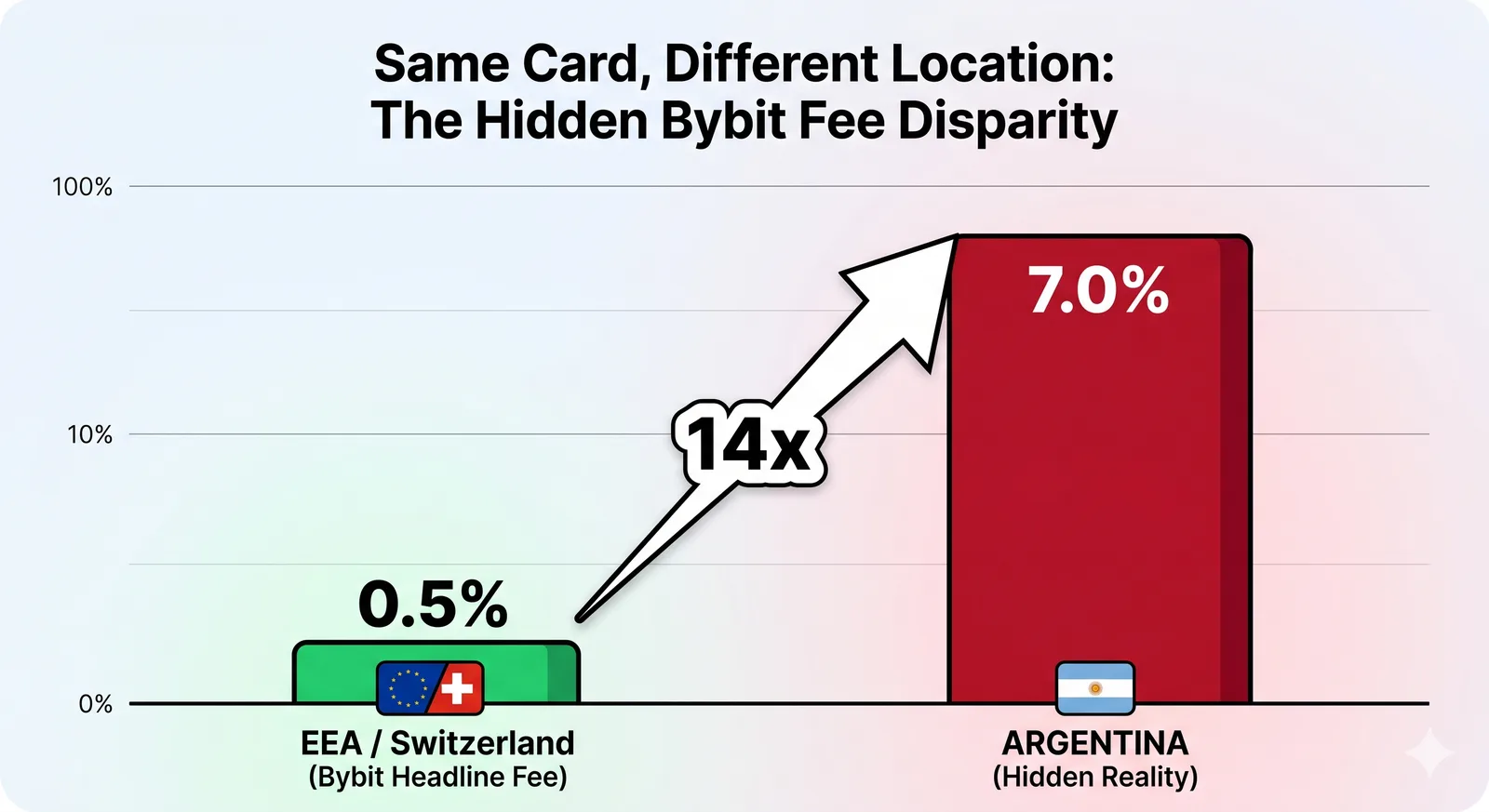

| Bybit | “0.5% in EEA” | 7% in Argentina, 2% APAC, 1.5% Brazil |

Bybit is the clearest case. That “0.5%” number only applies to EEA, Switzerland, and Mexico. Live in Argentina and you pay 14× that. The landing page does not say so.

Everything above came from reading documents. That method has a hard ceiling, and it took a card in my own hand to see where it sits. On 28 July 2026 I bought something priced at one euro on the Tria Card and watched what the statement did with it.

One euro settled at $1.16. Tria itemises its charges better than almost any card I have used, and the itemisation still does not add up: the two fees it names, Visa’s 1% and its own 0.50%, come to 1.50%, while the real distance from the interbank rate was 2.64%. The missing 1.12 points are inside the exchange rate itself. Tria settled at 1.1494 USD/EUR on a day the European Central Bank reference rate was 1.1367.

That gap appears on no line item, in no fee schedule, in no help-centre article. Ctrl-F would never have found it. It is not an accusation of overcharging either, since Tria advertises up to 3% and 2.64% is inside the claim. The narrower point is the one that matters for this guide: a card can be truthful about its ceiling and still route the largest single component of your cost through a channel that has no name on your statement.

For contrast, the other card I hold and spend on, the Ether.fi Cash Card, charges 0% FX on euro purchases and settles euros out of a dollar balance. Two Visa cards, both self-custodial, both honest in their marketing, and a difference that only shows up once someone buys something. The screenshots behind this measurement are on the Tria card page, and the rest of what we have measured ourselves is in advertised vs measured.

No hidden spread, no “conversion” euphemism, no regional gotcha I could find:

If the card you want is not on that short list, do not trust the landing page. Two steps:

Whatever comes up is your real cost. The “best crypto card” depends entirely on where you live and whether you read the fine print. The full dataset is on Sweepbase. You can filter 138 live cards by real FX fee and see the hidden costs side by side.

For a deeper walk through every fee type, see our crypto card fees guide. If you want a ranking that already factors real FX cost into a score, read Top 10 crypto cards by real fees.

The numbers in this section are an April 2026 snapshot, taken when the Sweepbase database held 141 cards; the catalog has grown since, but we have not re-run that audit. “0%” means no issuer markup on top of the standard Visa/Mastercard network rates, which are roughly 1% for USD-settled cross-border transactions and 1.4% when settled in another currency. Numbers come from each issuer’s published fee schedule or Terms of Service. When an issuer discloses a different number for different regions, the table above quotes the range. Fees change, so verify against the live fee schedule before applying for any card.

The Tria figure is the exception: it was measured on a purchase rather than read out of a document, against the ECB reference rate for that day. How we do that, and what we refuse to claim from a single purchase, is written up on how we test.

Editorial commentary from Mihail B.. Half of the “hidden FX” cases above turned up because a reader emailed us when their actual statement did not match the marketing page. The other half came from us reading fee schedules ourselves.

Visa and Mastercard charge interchange and assessment fees in fiat. Issuers receive the merchant's fiat side of the transaction, then have to source that fiat from the user's crypto balance. The cost of that conversion has to land somewhere, settlement spread, prepaid top-up fee, or an explicit FX line. When marketing teams strip “FX” from the landing page, accounting teams move the same number to a different line. That is the entire mechanism. It is not malicious, it is mathematics, but the result for the cardholder is identical to a fee.

When you read a fee schedule for a card whose marketing claims 0% FX, the cost is almost always under one of these labels: stabilization fee (some self-custody products), card spend fee (1inch and similar wallet-funded products), or conversion spread (most exchange-issued cards). If none of those phrases appear, the cost is absorbed by the issuer's interchange revenue and the card sits in the group we treat as honest.

The Bybit case in the table is not unique. Several issuers charge 0.5% in EEA, Switzerland, and Mexico, then 1.5–7% elsewhere. The headline rate on the global landing page is the rate that applies to whichever market they want to acquire users in this quarter. If you live outside that market, your fee is higher and you have to dig into the regional fee schedule to find it. Read the schedule for your country, not the international one.

The picture is shifting for 2026. MiCA in the EU is forcing issuers to publish a clearer fee summary, which should compress the gap between landing-page and reality on the EU-licensed cards we track. Separately, several US-issued cards (notably Coinbase One Card and Gemini Credit) have moved their crypto-conversion fee out of the FX line and into a clearly labelled “asset purchase fee” so that spending fiat-funded balances really does cost zero. We will refresh this analysis every quarter as the 170-card dataset shifts.

Every card above has its own page with the live fee schedule, cashback rate, and custody model. Filter the full catalog by region, network, and fee structure to find the card that fits how you actually spend.

Every claim above is grounded in a primary source. The list below is what we read to write this guide: regulators, issuer fee schedules, archived snapshots. If a number looks wrong, start here.

Fee changes, new cards, cashback drops — delivered weekly. Plus a free PDF: Top 10 Crypto Cards Ranked by Real Fees.

No spam, ever. Unsubscribe anytime.